Dwelling Landlord

Storm after storm, year after year®, we are here for you. We have options for every type of homeowner.

Dwelling Fire Insurance for Landlords

A Dwelling Fire Landlord (DF3-DL) policy is considered à la carte because it offers flexible coverage options to owners of rental properties. A Dwelling Fire Landlord policy provides basic coverage for the structure of the insured dwelling (a 1-4 family home).

You have the option to include coverage for theft, ordinance or law, premises liability, and medical payments.

Dwelling Fire Coverage for Your Rental Home Includes

Many coverages have a minimum and maximum coverage amount (commonly referred to as “coverage limit”). Each of the coverage tabs below provide a basic overview of the coverage and the applicable coverage limits.

DF3-DL Coverage for the

Structure of Your Home

A Dwelling Fire Landlord policy provides coverage for damage to the structure of your dwelling in the event of a covered loss. Coverage A includes Replacement Cost for covered losses. This means that the structure of your home is valued using today’s construction costs to rebuild or repair your home, which is not the same as the real estate value.

Homes with an older roof that may not be eligible for a standard Homeowners Insurance policy could be eligible for a Dwelling Fire Landlord policy because the Dwelling Fire program has a Roof Surfaces Payment Schedule that can be added to the base policy.

Dwelling (Coverage A) Limit: $125,000 – $5,000,000

A higher minimum coverage limit applies to properties located in certain counties.

DF3-DL Coverage for

Other Structures

Our Dwelling Fire Landlord policy provides coverage for “other structures” located on the residence premises. For example: a detached garage or in-ground swimming pool may be considered an “other structure”. Additional coverage is also available for pool enclosures.

Other Structures (Coverage B) Limit: 1% – 20% of Coverage A

DF3-DL Coverage for

Your Contents

Coverage C is available for the property you own in the home. Some examples of the contents you may elect to cover are furniture and appliances. Coverage C does not include coverage for your tenant’s personal belongings.

Personal Property (Coverage C) Limit: $0 – $250,000

Actual Cash Value is the only loss settlement option for personal property on a Dwelling Fire Landlord policy.

DF3-DL Coverage of

Loss of Use

If your rental property becomes uninhabitable due to a covered loss, your landlord insurance policy provides coverage for the loss of rental income you incur while the home is uninhabitable.

Coverage D & E Limits: 10% of Coverage A

DF3-DL Coverage for

Personal Liability on Your Property

Premises Liability can protect you in situations that may be unforeseen, such as a visitor twisting their ankle on a loose step. Liability coverage also covers certain defense costs – even if the lawsuit filed against you is false, groundless or fraudulent.

Premises Liability Insurance (Coverage L) Limits: $0, $100,000, $200,000, $300,000, or $500,000

This valuable coverage is also available for properties deeded in the name of a Trust, LLC, or Estate.

DF3-DL Coverage for

Medical Payments

This coverage is paired with Personal Liability coverage to provide medical expense coverage to others if they are injured on your property.

Medical Payments (Coverage M) Limits: $0, $1,000, $2,500, or $5,000

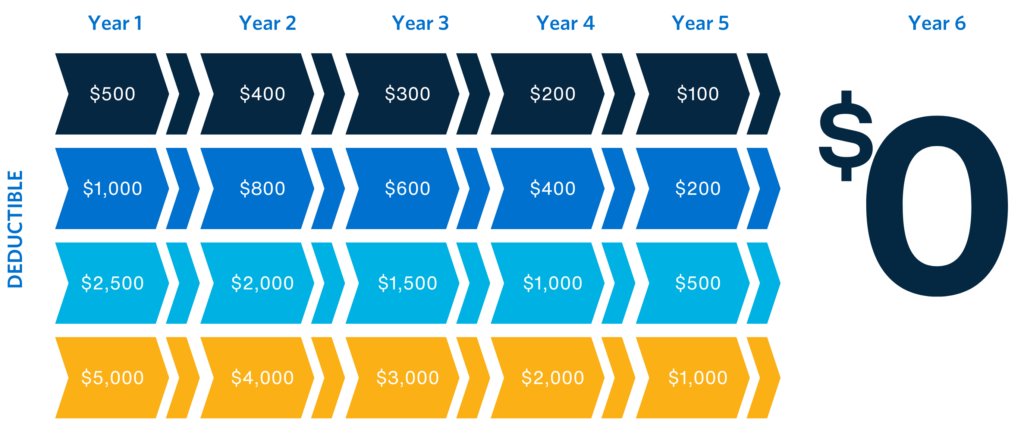

Dwelling Landlord (DF3-DL)

Disappearing Deductible

The Disappearing Deductible endorsement rewards you for being claims free by reducing your AOP (All Other Perils) and Water deductibles by 20% each year. This automatic endorsement applies to AOP and Water deductibles only and does not affect the Hurricane Deductible. Terms and conditions apply.

Optional Add-Ons

- Aluminum Screened Enclosures & Carport

- Identity Theft Protection & Monitoring

- Ordinance or Law

- Personal Property Theft

- Equipment Breakdown & Service Line Endorsements

- Water Back Up and Sump Overflow

Compare Our Plans

Choosing the right coverage can be overwhelming with so many options available. Use the chart below to compare our most popular policies and find the one that fits your needs.

- Dwelling Landlord (DF3-DL)

- Dwelling Basic (DF1)

- Condo (HO6)

- Dwelling Owner (DF3-DO)

- Signature+ (HO3)

- Premier (HO5)

‡ Two-night minimum required (DF3-DL)

† Two-night minimum required (HO6, DF1)

† Two-night minimum required (HO6, DF1)

- Dwelling Landlord (DF3-DL)

- Dwelling Basic (DF1)

- Condo (HO6)

- Dwelling Owner (DF3-DO)

- Signature+ (HO3)

- Premier (HO5)

‡ Two-night minimum required (DF3-DL)

† Two-night minimum required (HO6, DF1)

† Two-night minimum required (HO6, DF1)

Kudos From Our Customers

“An insurance company that actually cares about its customers. A true unicorn in the insurance industry. After hurricane Matthew, while other insurance companies were praying their phone’s didn’t ring, Security First was calling every single customer in the affected area and asking if they can help. True compassion.”

– Kenneth from Port Orange, Florida

You hear a lot of nightmares with insurance companies, but this was not one of them. Thank you Security First.

I’ve been with Security First for about 10 years. I’m very happy with how the process is moving forward.

I have the best insurance company in the state. I know I do. Security First has been a delight to work with. They’re simply the best.

I barely even have time to think about it, and I’m getting another contact from Security First about the next step in the process.

I can’t say enough about Security First Insurance. We have friends and family with other companies, and I don’t think they’ve had what we’ve had through every storm, and that means the world.

It’s so encouraging to see those that care about their customers and their clients here, trying to help them get a claim started and get their lives back in order.

By that morning, I already had my claims number, they were already working on people to send out to take care of the tree, tarping the house, and getting an inspector … It’s been a real dream to work with them.

I wouldn’t use anyone else, honestly. It’s been a life-changing experience in terms of insurance.

They contacted us before the storm and after the storm to make sure that we were ok and had a place to go. We’ve recommended them to other people.

Security First has always come through. There’s security in Security First.

This is our third hurricane in 13 months, and Security First Insurance has been our homeowner’s insurance through all of them. I’ve had a really good experience.

I was shocked how quickly Security First reached out. So very happy we picked Security First for our home insurance.

Protect Your Home Today

We stand behind every policy we write, storm after storm, year after year®.

Our simple and convenient quote process makes it easy for you to get started. Take the first step towards protecting your most valuable asset by requesting a quote today.